UPI Cash Withdrawal via QR Code: The Future of Cardless Cash at CSP Centers in India

Introduction: Transforming Cash Access in the Digital Age

India has witnessed a massive transformation in digital payments over the last few years. With the widespread adoption of UPI, transferring money has become faster, easier, and more accessible than ever before. However, while digital transactions are growing rapidly, the need for physical cash still remains strong, especially in semi-urban and rural areas.

To bridge this gap, a new solution has emerged—UPI Cash Withdrawal via QR Code at CSP centers. This service brings together the convenience of UPI and the practicality of cash, allowing users to withdraw money without needing an ATM card or biometric authentication. It is not just a technological advancement but a step toward financial inclusion, making cash access simpler for millions of users.

Understanding UPI Cash Withdrawal via QR Code

UPI Cash Withdrawal is a system that allows customers to receive cash by simply scanning a QR code generated by a CSP retailer. Unlike traditional methods that require an ATM card or AEPS-based fingerprint verification, this service leverages UPI infrastructure to complete the transaction.

At its core, the system works on a simple mechanism: the retailer generates a dynamic QR code, the customer scans it using any UPI app, authorizes the payment, and receives cash instantly. This seamless process eliminates dependency on physical cards and biometric devices, making it highly efficient and user-friendly.

The service is currently being enabled through the collaboration of NPCI and Jio Payment Bank, ensuring reliability, security, and smooth execution across supported platforms.

How the Process Works in Real Life

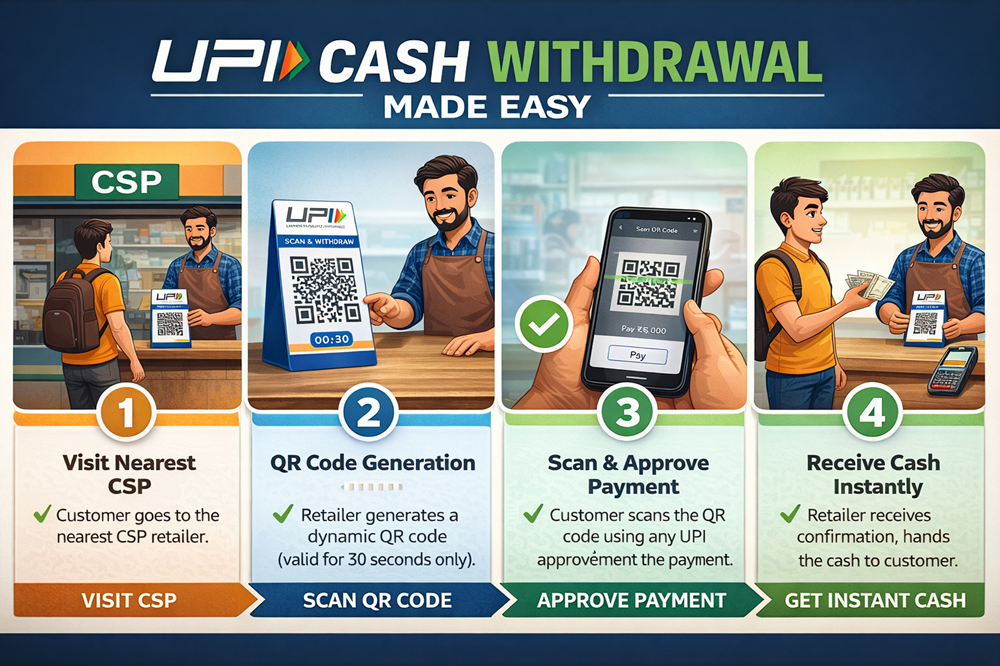

From a user’s perspective, the experience is straightforward and quick. A customer walks into a nearby CSP center and requests a cash withdrawal. The retailer then enters the requested amount into the system and generates a dynamic QR code.

This QR code is unique for each transaction and remains active for only 30 seconds, ensuring high security. The customer scans the code using their preferred UPI app, verifies the amount, and enters their UPI PIN to authorize the transaction. Within seconds, the retailer receives confirmation, and the cash is handed over to the customer.

This process removes multiple layers of friction that exist in traditional systems, such as card swiping, PIN entry on machines, or fingerprint mismatches. As a result, it significantly enhances the user experience.

Key Features That Make UPI Cash Stand Out

One of the most important aspects of this service is its simplicity. Customers do not need to carry any physical card or remember additional credentials beyond their UPI PIN. This makes it particularly useful for individuals who may not be comfortable using traditional banking tools.

Another major advantage is accessibility. Since CSP centers are widely available, especially in areas where ATM infrastructure is limited, users can easily find a nearby point for cash withdrawal. Additionally, the service works with all major UPI apps, making it universally compatible.

Security is also a strong pillar of this system. The use of dynamic QR codes, real-time transaction processing, and encrypted banking networks ensures that each transaction is safe and protected against fraud.

Transaction Limits and Operational Guidelines

While the service offers great convenience, there are defined limits in place to maintain operational control and security.

A retailer can generate a QR code for a maximum of 5000 INR per transaction. The total daily limit for transactions is capped at 10000 INR, while the monthly limit is set at 50000 INR. These limits are applicable at the retailer level and help in managing risk while ensuring smooth operations.

The dynamic QR code generated for each transaction is valid only for 30 seconds. This short validity period plays a crucial role in preventing misuse and ensures that each transaction is completed securely within a controlled timeframe.

Why UPI Cash is a Game-Changer for the Ecosystem

The introduction of UPI Cash is a significant development in India’s fintech landscape. One of its biggest advantages is that it reduces dependency on ATMs, which are often unavailable or out of service in many regions. By enabling cash withdrawal at CSP centers, the service brings banking closer to the customer.

It also addresses a common issue faced in AEPS transactions—biometric failure. Many users, especially laborers and elderly individuals, face difficulties with fingerprint authentication. UPI Cash completely removes this barrier, making transactions smoother and more reliable.

For retailers, the service requires minimal infrastructure. A smartphone with internet connectivity is sufficient to operate, eliminating the need for additional hardware such as biometric devices.

Benefits for Customers: Convenience Meets Accessibility

From a customer’s point of view, the benefits of UPI Cash are substantial. The ability to withdraw cash instantly without carrying a card or relying on biometric authentication adds a new level of convenience.

Moreover, the service enhances financial accessibility. People living in remote areas can now access cash without traveling long distances to find an ATM. The process is quick, secure, and easy to understand, even for first-time users.

Another important aspect is safety. Since users do not need to share sensitive details like card numbers or fingerprints, the risk of data misuse is significantly reduced.

Benefits for CSP Retailers: A New Income Opportunity

For CSP retailers, UPI Cash is more than just a service—it is a business opportunity. Similar to AEPS transactions, retailers can earn commissions on every successful transaction, creating an additional revenue stream.

The service also helps in increasing customer footfall. As more people become aware of this Facility, CSP centers will naturally see higher engagement. This increased traffic can lead to cross-selling opportunities for other financial services.

Additionally, UPI Cash acts as a reliable backup for AEPS. In situations where biometric authentication fails, retailers can still serve their customers using this alternative method, ensuring uninterrupted service.

UPI Cash vs AEPS: A Practical Comparison

While both UPI Cash and AEPS aim to provide cash withdrawal services, their approach is quite different.

UPI Cash relies on UPI PIN authentication, making it faster and less dependent on physical devices. In contrast, AEPS depends on fingerprint verification, which can sometimes fail due to technical or environmental factors.

From a device perspective, UPI Cash only requires a smartphone, whereas AEPS needs a biometric device. This makes UPI Cash more accessible and cost-effective for retailers.

In terms of reliability, UPI Cash generally has a lower failure rate, as it operates on the robust UPI infrastructure. This makes it a preferred option in many scenarios.

Security Framework of UPI Cash Transactions

Security remains a critical component of any financial service, and UPI Cash is designed with multiple layers of protection. The use of dynamic QR codes ensures that each transaction is unique and time-bound.

UPI PIN authentication adds another layer of security, ensuring that only the authorized user can complete the transaction. Real-time confirmation further reduces the chances of discrepancies or fraud.

Additionally, all transactions are processed through secure banking channels with encryption protocols, maintaining the integrity of user data.

Market Demand and Future Potential

The demand for UPI Cash services is steadily increasing, driven by the widespread adoption of UPI and the need for convenient cash access. As more users become comfortable with digital payments, services like UPI Cash will naturally gain traction.

Looking ahead, the future of this service appears promising. With potential increases in transaction limits, expansion to more banking partners, and wider adoption across service providers, UPI Cash could become a mainstream method for cash withdrawal.

It represents a perfect blend of digital innovation and practical utility, aligning with India’s vision of a digitally empowered economy.

Ezeepay and UPI Cash Service

Ezeepay has already adapted this UPI Cash service, enabling its CSP network to offer seamless and efficient cash withdrawal solutions to customers.

Conclusion

UPI Cash Withdrawal via QR code is redefining how people access cash in India. By removing the need for cards and biometric authentication, it simplifies the entire process and makes it more inclusive.

For customers, it offers speed, convenience, and accessibility. For CSP retailers, it opens up new avenues for income and business growth. As adoption continues to rise, this service has the potential to become a cornerstone of India’s financial ecosystem.

Final Thoughts

The evolution of financial services in India is moving toward solutions that are simple, secure, and scalable. UPI Cash perfectly fits this vision by combining the power of digital payments with the necessity of physical cash.

As awareness grows and infrastructure expands, UPI Cash is set to play a crucial role in shaping the future of cash transactions in the country.